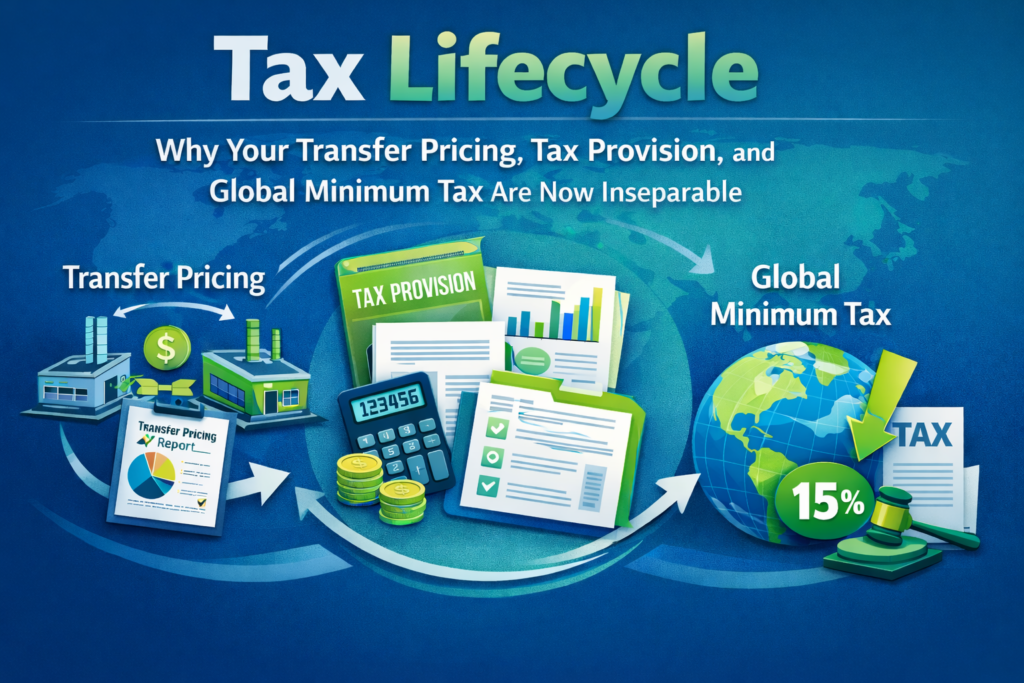

For years, tax departments have largely managed their functions in distinct silos. Transfer pricing specialists focused on intercompany transactions, tax accounting teams diligently worked on tax provisions, and international tax experts grappled with the ever-evolving landscape of global regulations. However, with the advent of the Global Minimum Tax (Pillar Two) and the increasing complexity of tax reporting, these three critical areas are no longer independent of one another. They are converging into an Integrated Tax Lifecycle, where the output of one directly impacts the inputs and outcomes of the others.

The common denominator? Data. And the need for unprecedented accuracy, agility, and visibility across your entire financial data pipeline.

The New Reality: From Silos to Synergy

Let’s break down why Operational Transfer Pricing (OTP), Tax Provisioning, and the Global Minimum Tax (GMT) are now inextricably linked:

1. Operational Transfer Pricing (OTP): The Foundation

OTP is about setting and managing the prices for transactions between related entities within a multinational enterprise (MNE). This includes everything from the sale of goods and services to intellectual property licenses and financial arrangements. Effective OTP ensures that these transactions are conducted at arm’s length, minimising audit risk and optimising the allocation of profits across jurisdictions.

The Traditional View: OTP was primarily a compliance exercise, often managed through year-end adjustments to align actual results with target margins.

The New Reality: OTP is now the real-time engine of your tax lifecycle. Every intercompany invoice, every cost allocation, and every profit split directly influences the financial results that flow into your general ledger. If your OTP isn’t executed accurately and consistently throughout the year, it creates a domino effect of issues down the line.

2. Tax Provisioning: The Measurement & Reporting

Tax provisioning is the process of estimating and accounting for income taxes in a company’s financial statements. It involves calculating current and deferred tax liabilities and assets, determining the effective tax rate (ETR), and providing disclosures in accordance with accounting standards (e.g., ASC 740, IAS 12).

The Traditional View: Tax provision teams would use year-end financial results (after TP adjustments) to perform their calculations.

The New Reality: The tax provision is no longer just a rear-looking exercise. It’s a forward-looking forecast that needs to anticipate the impact of OTP decisions and the impending GMT rules. Volatile or unexpected TP adjustments can drastically alter your ETR, making accurate quarterly provisioning a significant challenge. Moreover, the detailed financial accounting data used for the provision is the same data that underlies GMT calculations.

3. Global Minimum Tax (GMT / Pillar Two): The Ultimate Arbiter

The Global Minimum Tax, a key component of the OECD’s Pillar Two initiative, introduces a 15% effective minimum tax rate for large MNEs. If an MNE’s effective tax rate in a particular jurisdiction falls below this threshold, a “top-up tax” is triggered, payable either in that jurisdiction or in another.

The Traditional View: There was no global minimum ETR to contend with. Tax planning focused on optimising rates where possible.

The New Reality: GMT fundamentally changes the game. It’s not just about what your local tax rate is, but what your jurisdictional ETR is. And that jurisdictional ETR is calculated based on financial accounting numbers, heavily influenced by your OTP decisions and then measured through your tax provision process. Unexpectedly low ETRs, perhaps due to aggressive (or poorly executed) transfer pricing, will now result in a tangible, unavoidable top-up tax cost.

The Critical Connection: Data, Data, Data!

The convergence of these three areas highlights a singular, overarching need: a single source of truth for your financial data, granular enough to meet the demands of each function.

- OTP relies on real-time transaction data to ensure arm’s length pricing.

- Tax Provisioning consumes entity-level financial data to accurately calculate current and deferred taxes.

- GMT mandates the use of financial accounting data (with specific adjustments) to determine jurisdictional ETRs and top-up taxes.

If these data streams are disjointed, inconsistent, or lack the required granularity, your MNE faces:

- Increased Compliance Risk: Non-compliance with transfer pricing rules, inaccurate tax provisions, and miscalculated GMT liabilities.

- Higher Costs: Unexpected top-up taxes, penalties, and increased advisory fees.

- Inefficiency: Manual reconciliations, duplicated efforts, and delayed reporting.

- Lack of Strategic Insight: Inability to model the impact of different TP strategies on your ETR and GMT exposure.

Building the Integrated Tax Ecosystem

Transitioning to an integrated tax lifecycle requires a strategic approach, typically involving:

- Data Transformation: Investing in robust data management systems to centralise, standardise, and enrich financial data across all entities. This means bridging the gap between ERP systems, consolidation tools, and tax-specific platforms.

- Process Harmonisation: Breaking down departmental silos and fostering collaboration between transfer pricing, tax accounting, and international tax teams. Standardised processes ensure consistency and reduce manual handoffs.

- Technology Enablement: Leveraging tax technology solutions that can integrate data, automate calculations, and provide real-time analytics for OTP, tax provision, and GMT. This could involve advanced TP engines, tax reporting software, and Pillar Two calculation tools.

- Proactive Planning & Modeling: Using integrated data and technology to model the impact of different business decisions and transfer pricing strategies on your global ETR and potential GMT liabilities before they occur.

The era of isolated tax functions is over. Embracing the Integrated Tax Lifecycle isn’t just about compliance; it’s about strategic advantage. By connecting your operational transfer pricing, tax provisioning, and global minimum tax efforts through a robust data foundation, MNEs can gain unprecedented visibility, control costs, mitigate risks, and ultimately, navigate the complex global tax landscape with confidence.

Next steps

If your tax processes are still operating in silos, the risk is not theoretical. It is embedded in your data, your reporting, and your effective tax rate.

Start building your Integrated Tax Ecosystem today. Connect with our team to assess your current maturity and define the next concrete steps toward a fully aligned tax lifecycle.

Read more

Master OECD’s BEPS 2.0 Pillar Two Regulations with Wolters Kluwer’s CCH Tagetik

Staying compliant with the OECD’s BEPS 2.0. Pillar Two is more crucial than ever as regulations evolve. Time is running out for multinational corporations to ...

Read moreNavigate BEPS 2.0 Pillar Two with Confidence: Essential Solutions for Seamless Compliance

Over recent years, the emphasis in international tax law has increasingly shifted towards intensifying efforts to combat the strategies of tax avoidance and the...

Read more